Healthcare 1: Setting the Stage

Healthcare 1: Setting the Stage

An overview, especially for beginners.

If you've got the basics, feel free to jump ahead for more interesting content.

What is healthcare?

‘Healthcare’ is a really broad term for a sector that actually encompasses a number of smaller sub-industries relating to medical services. All of these stakeholders collaborate with one another to provide vital and beneficial services to the public.

Health systems, hospitals, and urgent care

These are places you can see a medical professional about your health. Dr. Phil, chiropractors, and the like don’t count, because they are definitely not real medical doctors. These organizations can either be publicly or privately owned. Some are “for-profit” while others are “not-for-profit”. Of the places you can go, The University of Pittsburgh Medical Center (UPMC) is the largest—it’s a nonprofit hospital, with over 85,000 employees (it grossed $9.8B last year).

Physicians & medical professionals

Nurses, doctors, medical researchers, and lab technicians work for hospitals and clinics. The labor force in this industry is enormous: according to the Bureau of Labor Statistics (BLS), more than 16 million Americans work in healthcare related professions.

That’s more than manufacturing, retail, and most other industries you can think of.

Pharmaceuticals

Biotech and big pharma companies produce medicine to sell to hospitals, pharmacies, and specialty pharmacies (which are just like normal pharmacies, but serve up some extra-special complicated meds). The largest players are Roche, Novartis, Eli Lilly, and Pfizer. You guessed it. It’s also a huge industry. McKesson made $208B and Pfizer made $51B of revenue last year. This is somewhat of it’s own industry, so we’ll get to it another time.

Medical & life science technology

Like biotech and big pharma, medical technology and device companies (e.g. Medtronic, Siemens, GE…) sell their products to hospitals, research facilities, pharmacies (and people). Medtronic’s revenue? $30B. Yep, huge industry. We’ll lump this in with big pharma and cover it in detail soon.

Diagnostic services

Blood tests, imaging, and genetic tests aren’t always done by your doctor or the hospital itself. For example, when you get your blood drawn, your doctor doesn’t take the vials to some backroom to analyze them. The doctor ships the samples to another company to do the analysis. You may not recall their names, but Quest Diagnostics and LabCorp (two of the largest players), bring in $7B and $11B a year, respectively.

Administrators & brokers

There’s an enormous layer of price negotiations, payment agreements, patient tracking, and about a million other “administrative tasks” that happen in the backend every time you go to the hospital. Some administrators work directly for hospitals or clinics or insurers. Sometimes, a hospital, insurer, or employer will also hire an external company that specializes in healthcare administration or brokerage to do this work on their behalf (aka third-party administrators/TPAs). These orgs don’t have much of a public brand presence. Although, unheard of doesn’t mean unprofitable. At the larger end, these companies (like Crawford & Co.) can bring in well over $1B a year. Hope you’re following the “healthcare is ginormous” trend.

Health insurance & payment programs

Healthcare is one of the only industries where the person receiving a product or service doesn’t usually pay for it themselves. Typically, you or your employer pay a health insurance company a small fee on a regular basis instead. When any health expense comes up, the insurer will cover it. The point of this is so you don’t risk having to pay for really expensive care if you become severely ill. If you’re following the law (aka the ‘Individual Mandate’), you have an insurance plan: you might be covered by Kaiser, UnitedHealth, Aetna, Medicare, Medicaid, or maybe by your employer who runs their own insurance program. Insurers are even bigger (from a revenue perspective, anyway) than the other stakeholders we’ve mentioned so far. For example, UnitedHealth made $240B of revenue and $13B of profit last year. Keep in mind, Facebook made $70B and Google made $113B of revenue in the same period.

Health IT and Software

EPIC is a pretty ill-fitting name for the software that hospitals use, because it is in fact, far from it. It’s usually used to input patient data and store it. Most medical workers and health professionals are familiar with the computer program. It’s complicated, it’s outdated, it’s clunky, and every hospital runs its own slightly different version. There are a gazillion other tools and softwares within the system, but EPIC is the most important one.

In Fact’s Healthcare Series is going to cover each of these topics in detail. We’ll start with definitions for basic healthcare terminology and dive into the nuances of the value chain for each of these segments.

You may have heard, it’s expensive

Healthcare cost per capita in the United States soars above that of almost every other developed nation. You might think that means we’ve got the best of the best. Nope. Sadly, most of our measures of “national health” stagnate far behind those of our peer countries. In 2017 alone, the U.S. spent $3.5 trillion on healthcare (that’s an astronomical 17% of our GDP). And that was even before COVID-19. That means that when you add up what U.S. governments, insurers, you, me, and my mom are spending on healthcare, it averages out to about $10,739 per person each year (Centers for Medicare and Medicaid Services, 2018).

How does that compare? The U.S. spends roughly twice as much as other developed countries. When I say that healthcare outcomes fall dramatically short, I mean people are dying at higher rates than our experts would like and we’ve got a greater disease burden than in other countries (which you’ll see in Figures 1-3 below). That’s not to say that our health system is necessarily the direct root cause. Rather, the salient point here is that we’re spending an astronomical amount of money for how our health is faring.

We’ll eventually dive deeper, come up with some theories on this, and look at the expert (and not-so-expert) opinions out there.

Figure 1. The U.S. spends more than double what peer nations do. (Inflation adjusted)

Data Source: Kaiser Family Foundation

Figures 2 & 3 measure health outcomes in “disability adjusted life years” (DALYs) per 100,000 people. That’s the number of years that a group of 100,000 Americans lose to an illness or early death. One DALY is the equivalent of losing one year of healthy life to disease or death from your life expectancy (e.g. if the average person’s life expectancy in the U.S. is 80 years, and they only lived until 60, they lost 20 DALYs). When you sum DALYs across a bigger population, it tells you the gap between where our population’s health is, compared to where we expect it to be.

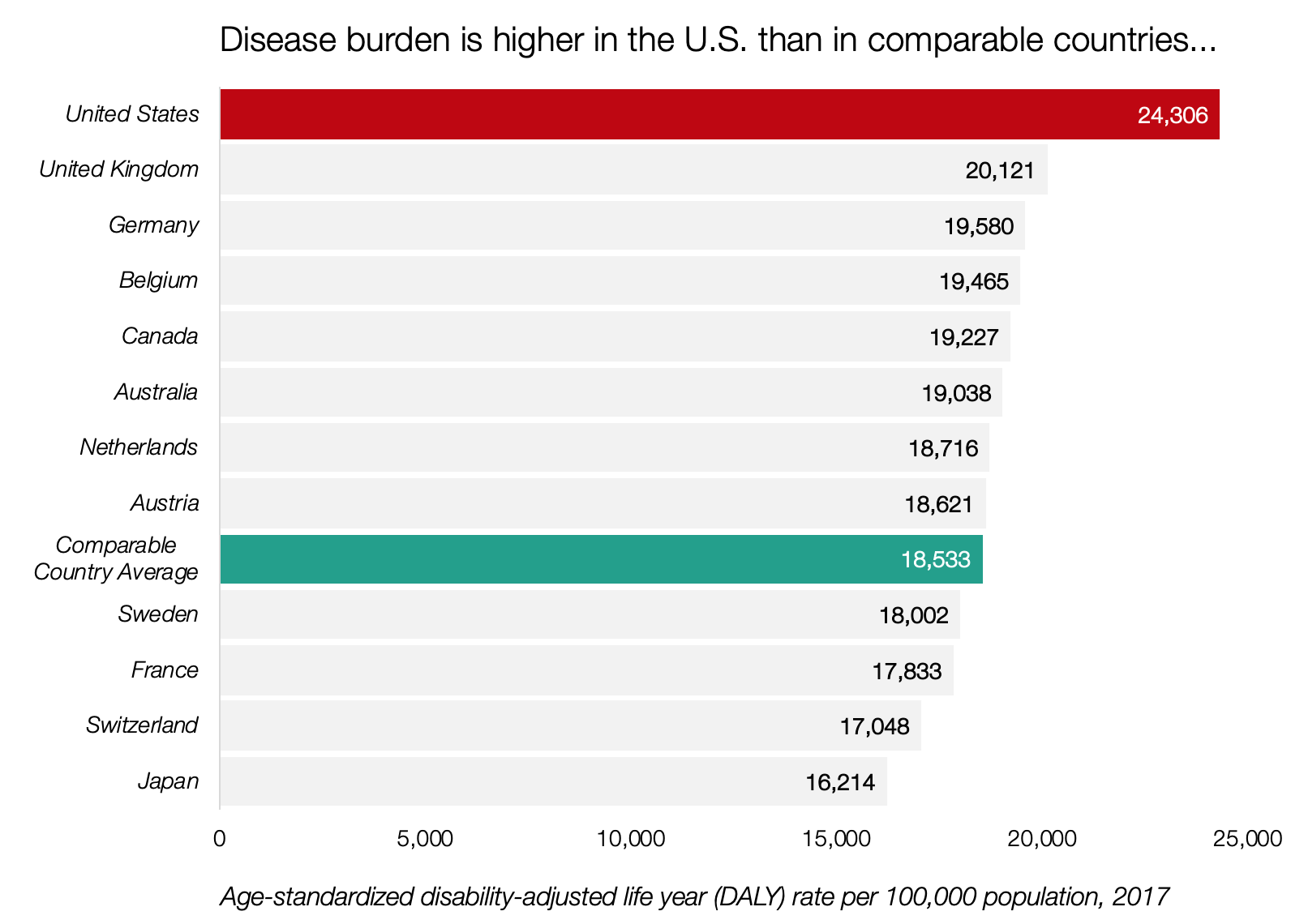

Figure 2. Despite the exorbitant spending, the U.S. still sustains a higher disease burden than peer nations.

Data Source: Kaiser Family Foundation

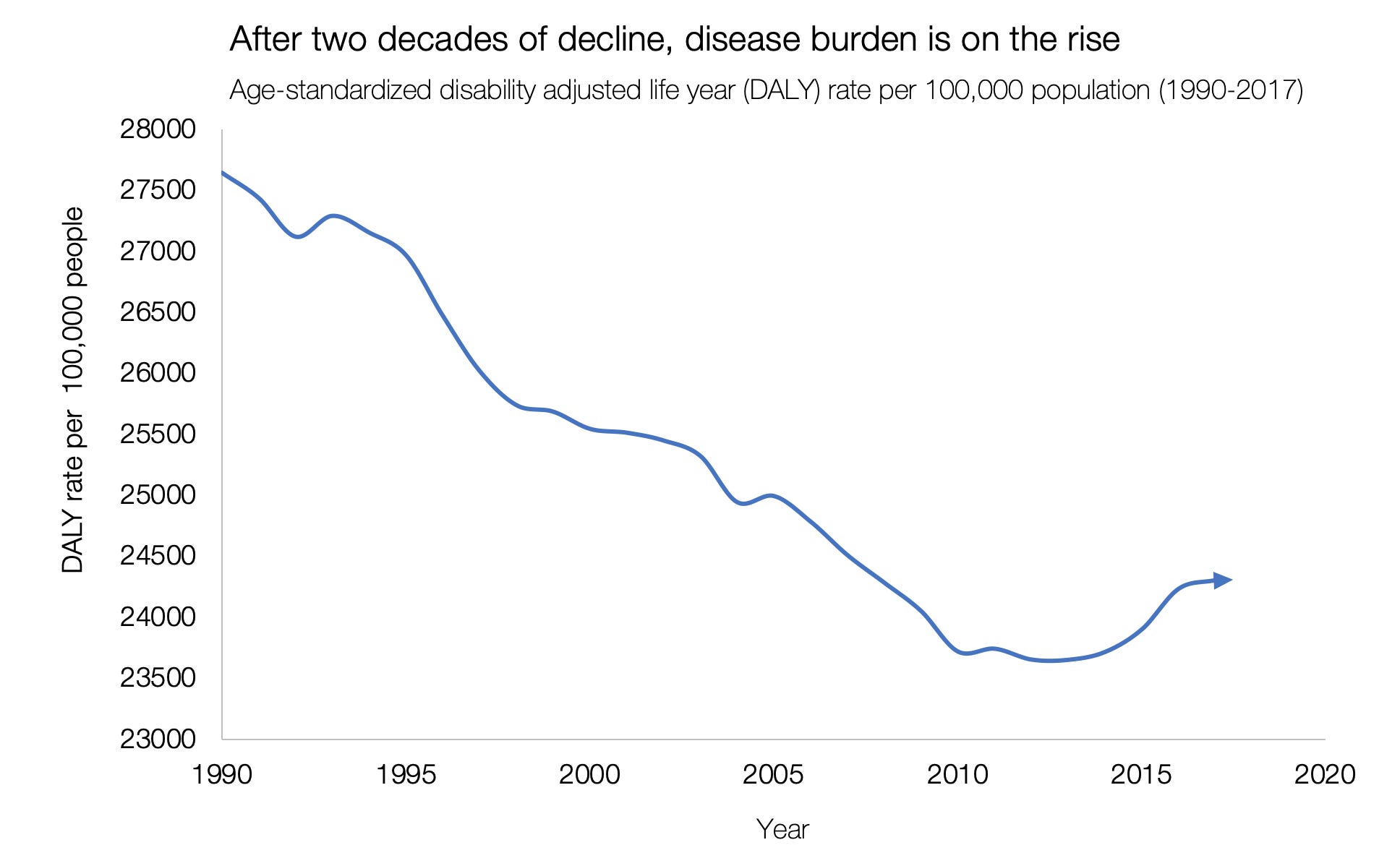

Figure 3. Disease burden is on the rise after decades of steady decline.

Data Source: Kaiser Family Foundation

Please keep in mind, that this increase in disease burden does not imply that healthcare is ineffective or unhelpful. It just gives rise to some questions about our health system. The good news, on the other hand, is that a number of trends show that new drugs, new medical devices, better hospital practices, and increased healthcare access have improved the health of Americans over the years (although, not by as much as we’d hoped). It might seem obvious that better medical treatments make people live longer, but it’s actually an enormous systemic effort to collect all the individual level data and monitor the overall health of the American population.

The 10,000 ft View

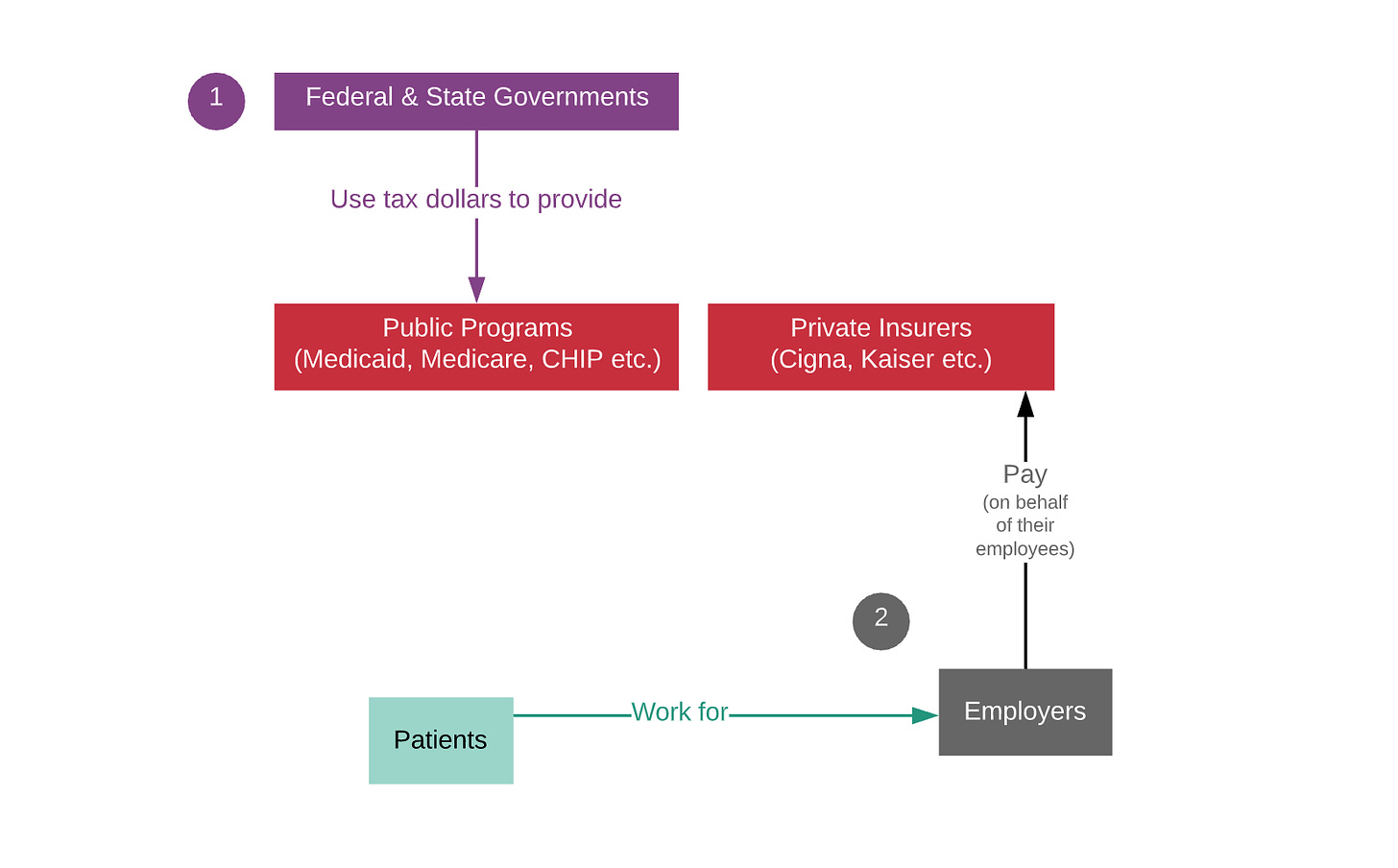

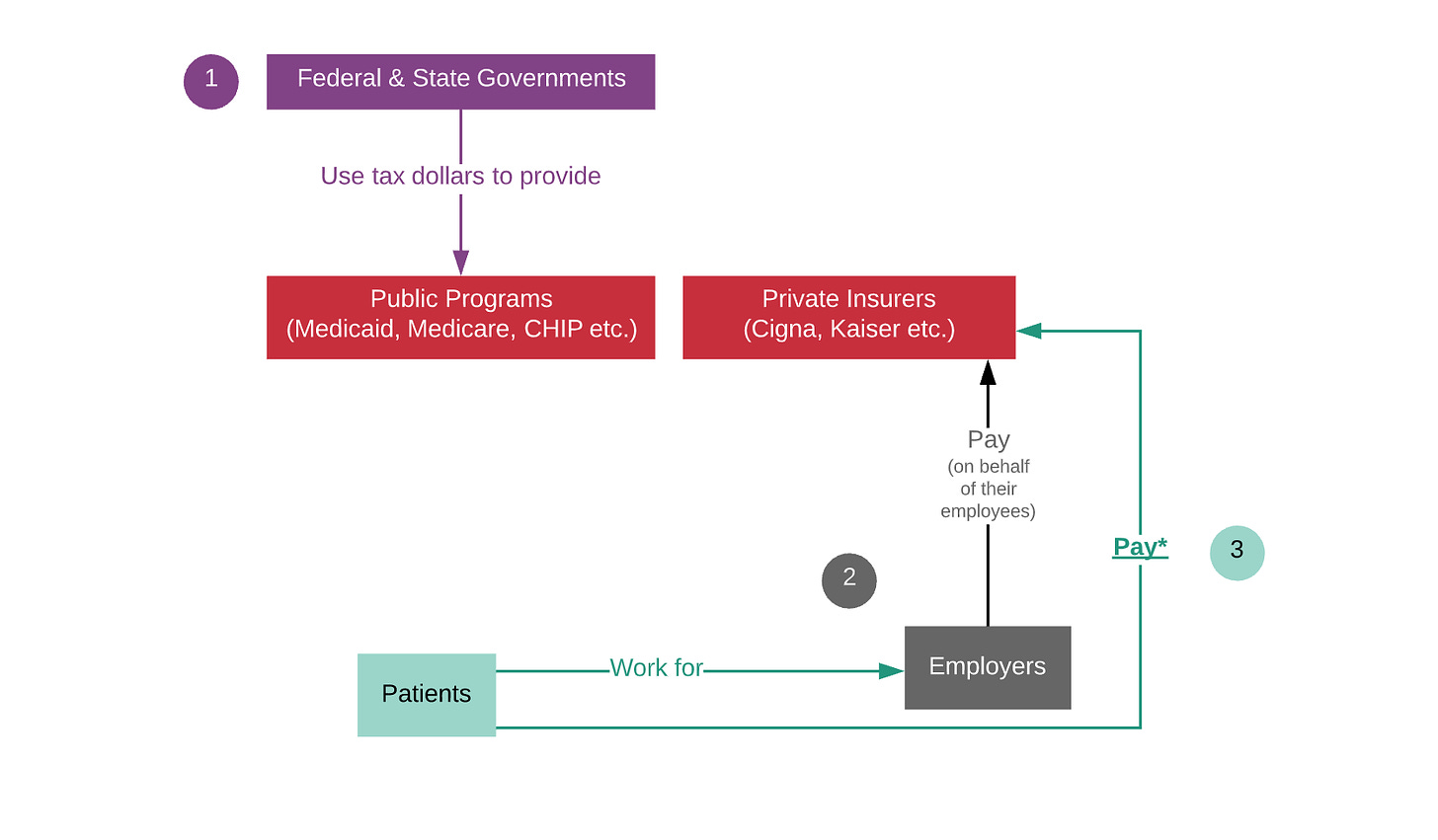

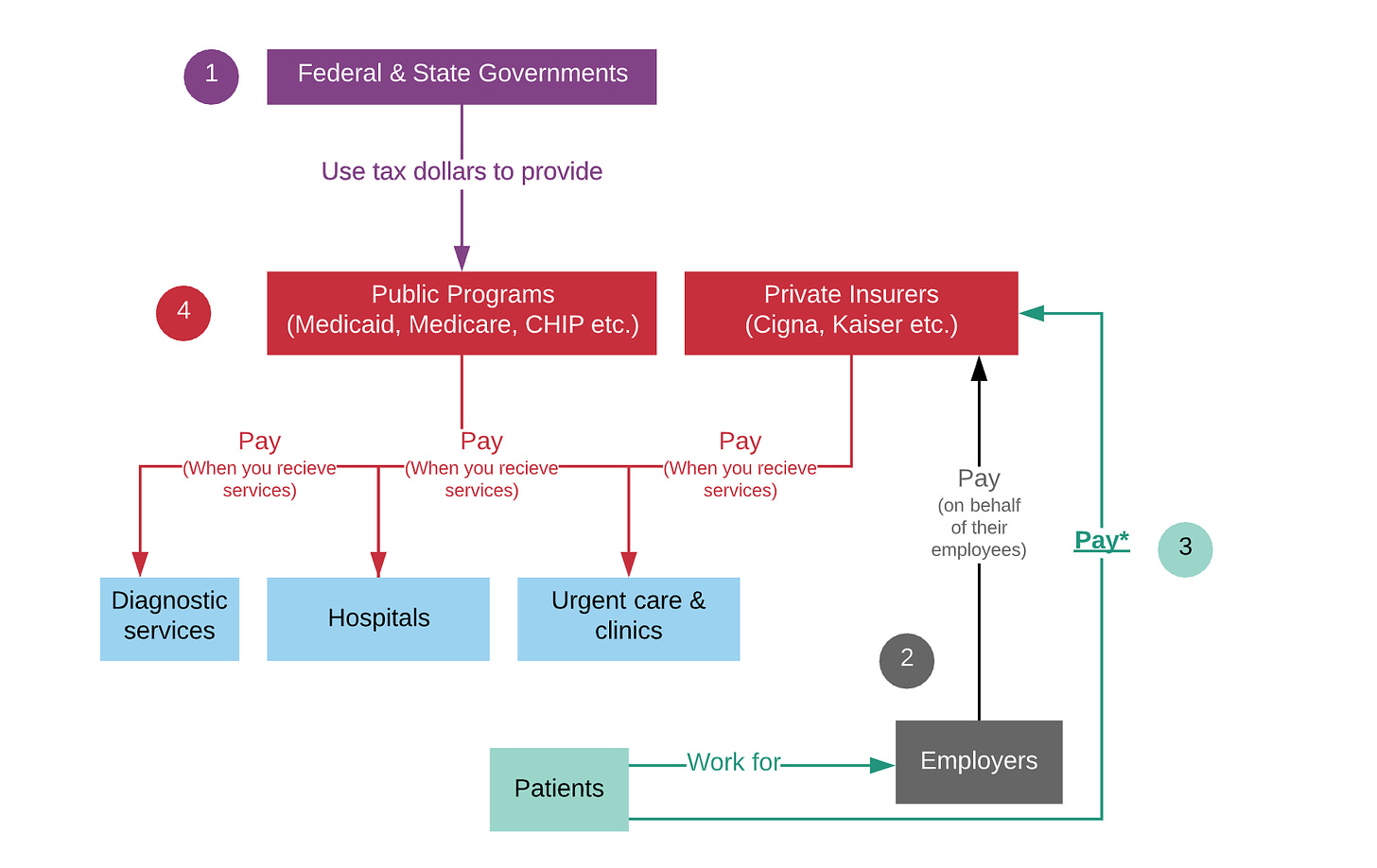

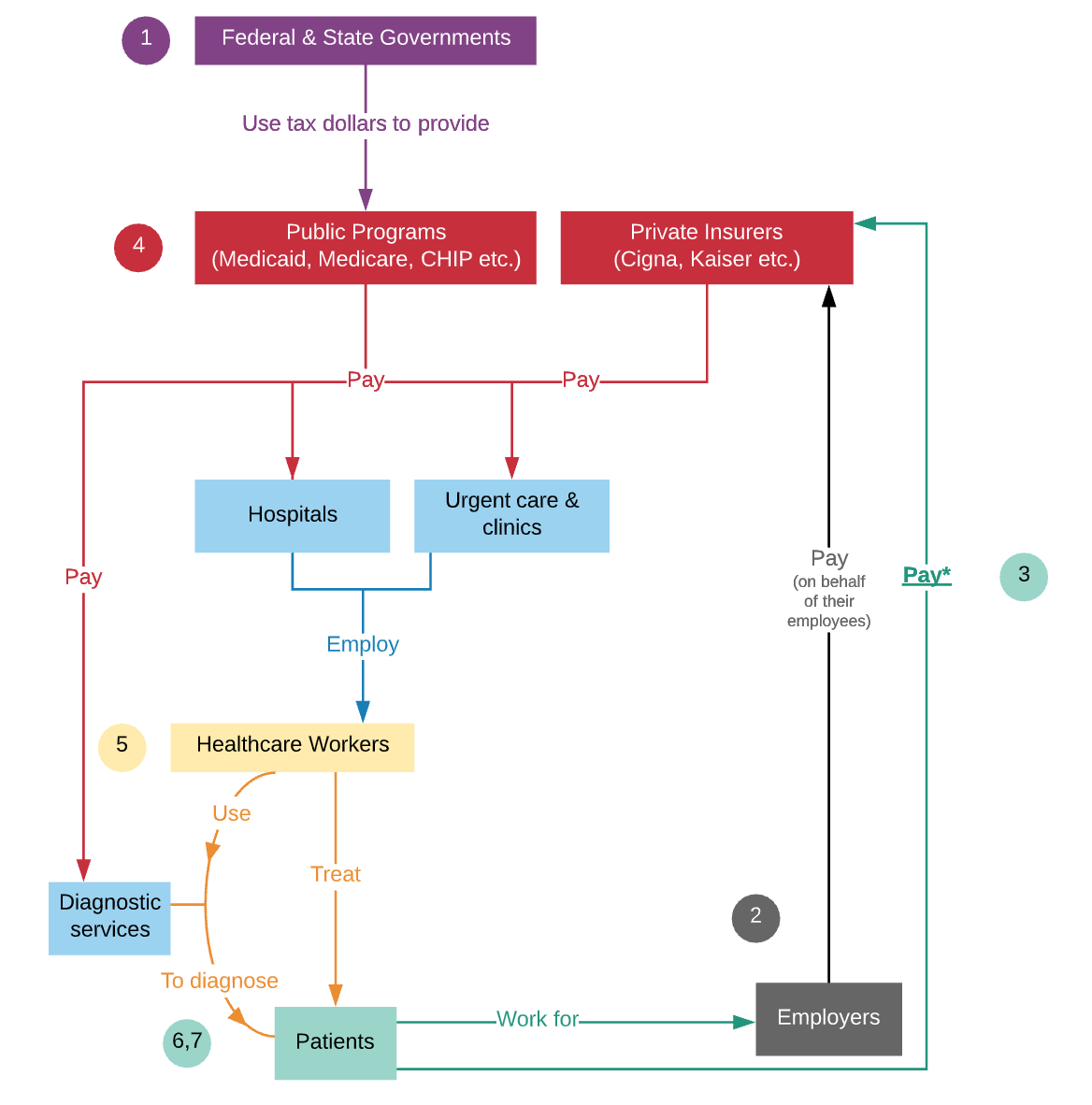

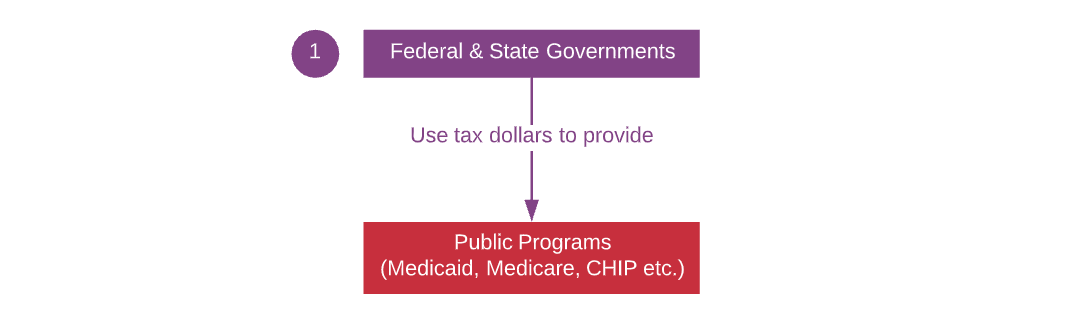

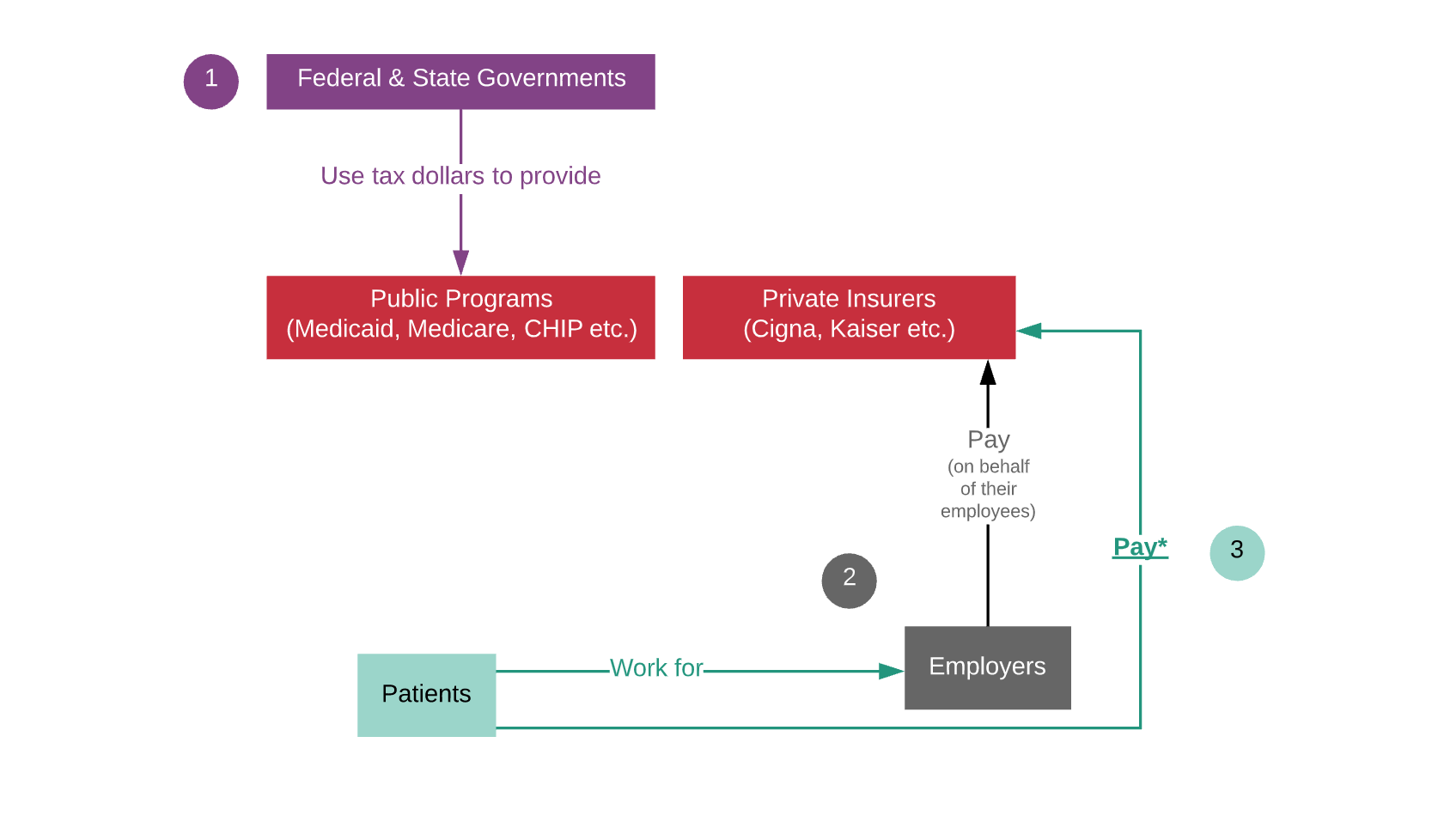

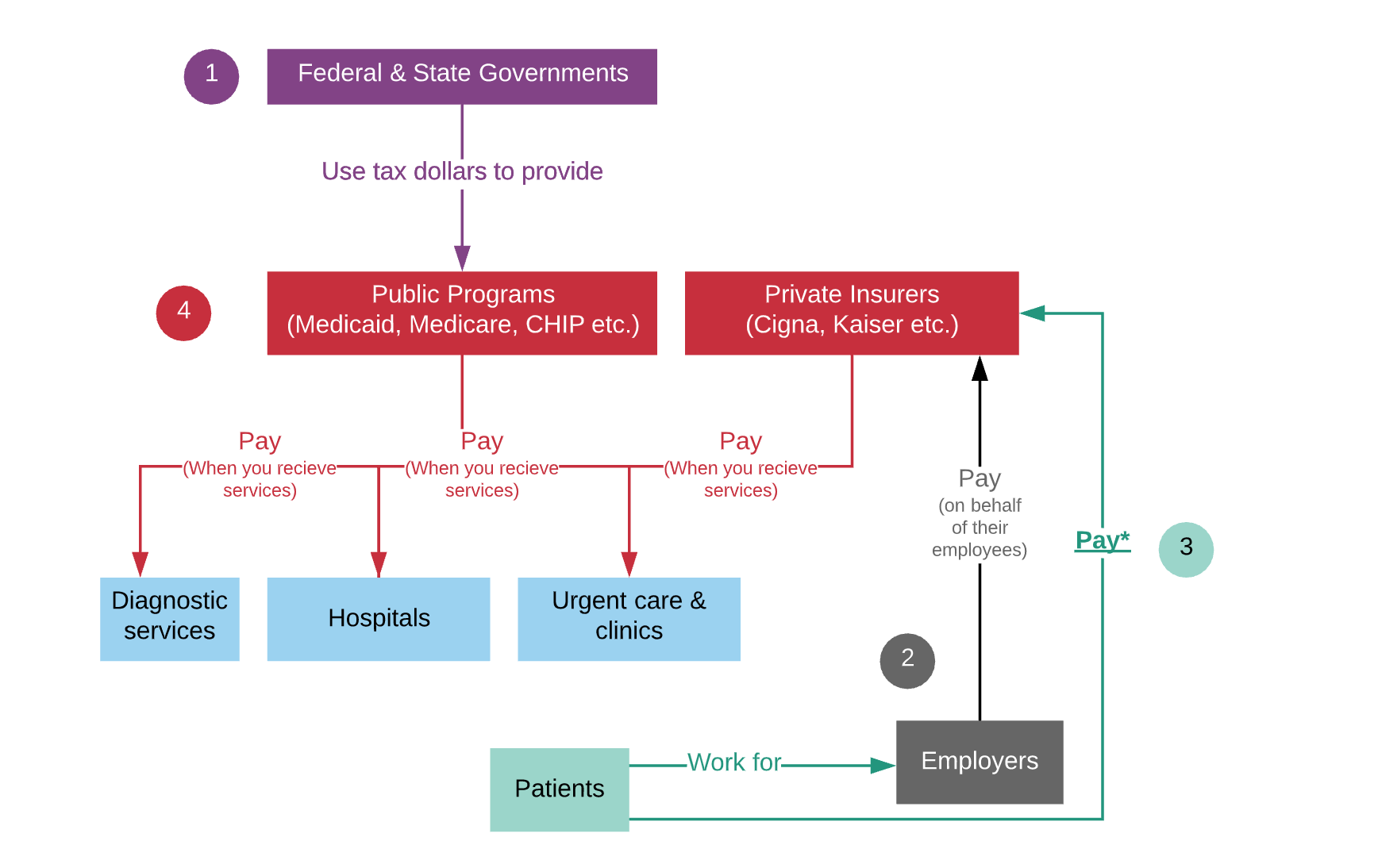

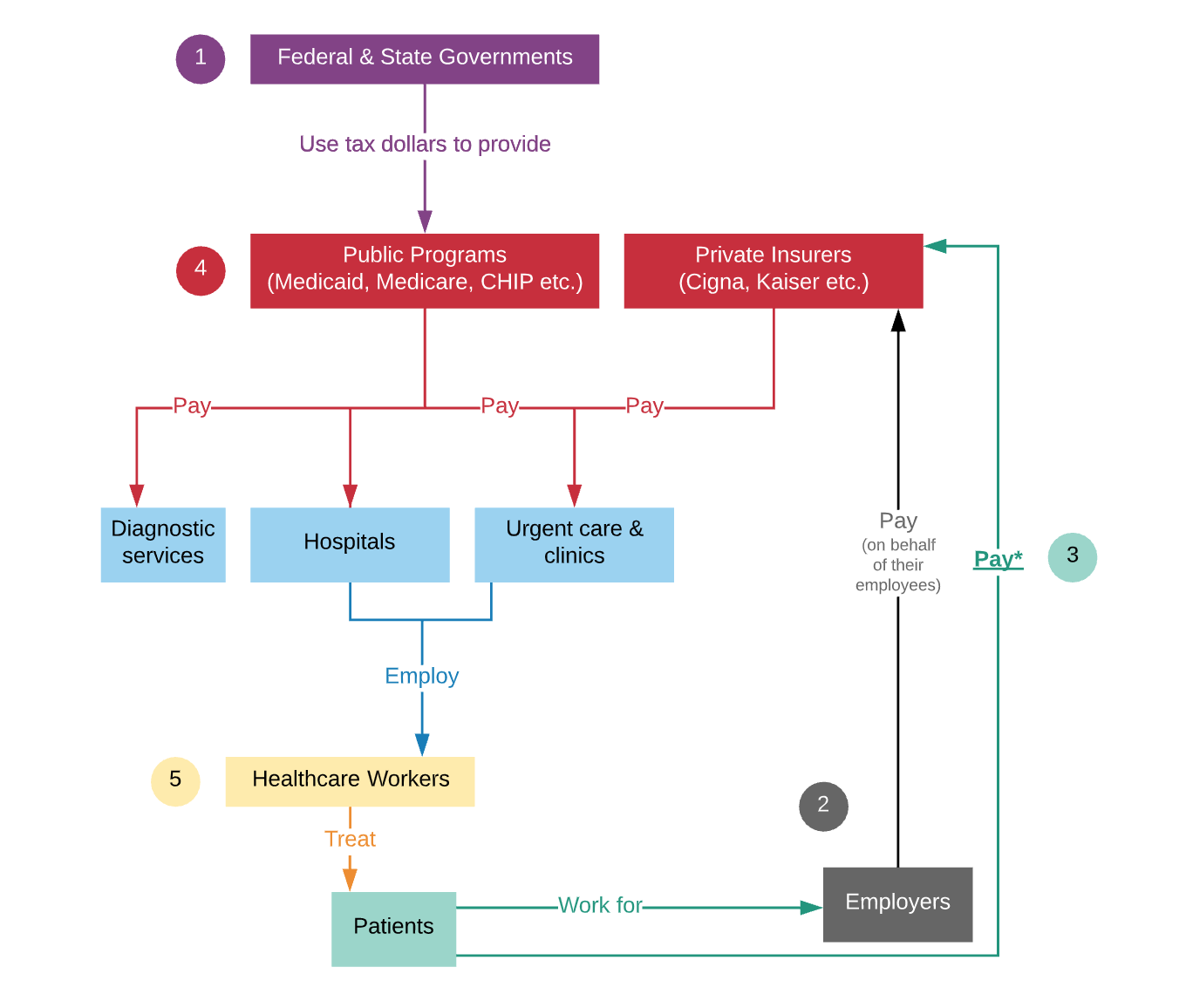

Federal and state governments pay for about half of all healthcare expenses in the U.S. (through programs like Medicaid and Medicare). Eligible individuals enroll in these programs to get healthcare coverage. These programs are managed by the Centers for Medicare and Medicaid services, Veterans Affairs, and other state government agencies.

Employers pay private insurers (like Cigna or Kaiser) on behalf of their employees. Larger employers also run their own internal insurance program if they think that they can lower costs by paying your medical expenses directly instead of paying an insurer to take care of it — these are known as self-insured employers.

Individuals who can’t get insurance through their employer pay for insurance plans on their own. Typically people can purchase a plan directly or go to an online insurance marketplace (a state government-run website that sells insurance plans).

Insurers and public programs pay hospitals, urgent care clinics, and diagnostic centers (and doctors) whenever one of their patients receives medical care or tests. There is an intricate backend system that insurers and hospitals use to determine prices and payment (we’ll save that for another day.)

Hospitals and urgent care clinics employ doctors and healthcare workers. Some doctors also own their own private clinics. There is also an important layer of administrative work and IT infrastructure within each of these organizations (we’ll also cover this in the future).

Healthcare workers and doctors see patients to diagnose or treat (or refer them other doctors.)

Doctors use third-party diagnostic labs to figure out exactly what illness you may have. For instance, when you go in for your annual check-up and blood test: your blood is drawn in the doctor’s office and shipped to a company like Quest Diagnostics. Quest then performs analyses and sends results back to your doctor. Your doctor will review the information and relay the results of this ‘diagnostic test’ to you.

Once you’re diagnosed, a physician might prescribe you medicines. The doctor sends your prescription to your preferred pharmacy, where you can retrieve the meds. When you pick up a prescription, your insurer pays for a portion of it, while you pay the rest (aka a copayment).

*In addition to paying for an insurance plan, patients also pay for their visits out-of-pocket directly to the provider that is giving them care. This is a copay or co-insurance.

**The relationship between pharmacies and insurers is actually a lot more complicated and involves third-party price negotiators (known as PBMs). We’ll cover the exact relationship between drug manufacturers, wholesalers, PBMs, and insurers in a future article.

Here are some topics we haven’t covered in this high-level chart, but will eventually…

a) How drugs are produced and how pharmacies or hospitals buy them

b) How medical devices are produced and how hospitals buy them

c) How insurers negotiate and pay for drugs, medical devices, and services

d) The IT infrastructure sitting behind healthcare organizations

e) How brokers sit between healthcare organizations and facilitate interactions, negotiations, and payments

f) How billing and payments in healthcare work

g) How physicians interact with each other

h) How federal and state governments regulate all of these healthcare related industries

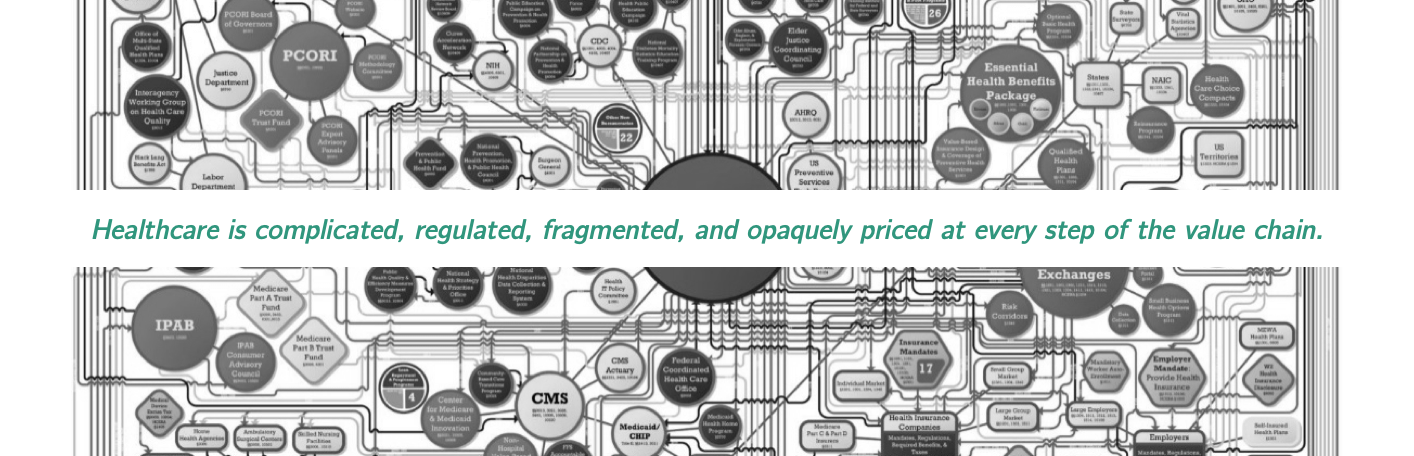

Why it’s so complicated…

At the most oversimplified level, there are arguably four main causes for complexity within healthcare:

Source: Patient Protection & Affordable Care Act, P.L. 111-148; Health Care & Education Reconciliation Act, P.L. 111-152 Prepared by: Joint Economic Committee, Republican Staff Congressman Kevin Brady, Senior House Republican Senator Sam Brownback, Ranking Member

It’s a heavily regulated industry. Pharma/medtech companies, insurers, hospitals, health systems, drug manufacturers, diagnostic labs, and most other entities in this industry are overseen by government agencies and regulatory bodies (e.g. the Food and Drug Administration, Center for Disease Control, Centers for Medicare and Medicaid Services etc.) Yes, there are a ton of laws, compliance organizations, and public officials trying to do the right thing. But don’t get too excited, because that doesn’t necessarily mean that all these regulations and policies always address the right issues or that they’re effective. Despite how regulated this industry is, there are actually a whole lot of gaps. On one end, laws that aren’t somewhat comprehensive leave big loopholes that allow rampant fraud and abuse to persist across our system (within hospitals, pharma companies, insurance companies and more). On the other hand, there are also a number of regulations that are so stringent that they stifle innovation and the progress that’s happening within healthcare. There are just so many issues to cover here, so we’ll have to dig into them slowly in future pieces.

Privacy. Data privacy is an important priority for healthcare entities. According to the law, they need to carefully protect sensitive information about patients, providers, hospitals, and insurers by storing it and transmitting it in certain ways. This need for privacy, when combined with outdated IT systems, prevents information from being exchanged and analyzed efficiently by those who need it to run the healthcare system smoothly. The format the data is collected in, the software it’s collected on, the mismatched way that it sits on different computers all cause much disfunction and inefficiency.

Pricing opacity. Individuals and payors often do not know precisely how much they will end up paying for healthcare services until after they are delivered. Often, prices are hidden between parties, negotiated by other intermediate parties, or resolved on unreliable timelines (e.g. long after a healthcare service has already been received).

Misaligned incentives. There are many, but we’ll start with one example here. Individuals who require healthcare services are rarely the ones who pay for it. Thus, the group that pays for the care and the person who receives healthcare have different incentives. For example, a patient who has reliable and high-quality insurance is optimizing for their health outcome, or the quality of services they receive. The insurer, who pays for your care, is attempting to achieve two things: (a) improve your health outcome (to prevent you from needing care again in the future); and (b) lower cost of your care (to lower their immediate expenses on you). So, if there’s a slightly better drug or procedure, but it costs way way more, the insurers incentives are not aligned with yours.

Quality and consistency fluctuate. The variance between health systems, clinics, healthcare workers, and physicians is difficult to observe or control. We don’t have any reliable or quantitative ways to monitor “patient health”, especially once you leave the hospital. It’s entirely possible that the lower healthcare outcomes we’re seeing in the U.S. have more to do with our lifestyle, diet, or environment, than the type of healthcare we receive (Figure 2 & 3). There are so many confounding variables that it’s hard to say which aspects of the healthcare system are succeeding, and which ones are not. But, without ways of monitoring the variables that affect each patient’s life, it’s hard to say precisely what the problem is or figure out what to do about it. We also lack the infrastructure to monitor the performance of doctors and hospitals. Not being able to measure the “value” or “quality” of healthcare quantitatively is one of the reasons we’re not able to solve many systemic issues within the industry. For example, there continues to be a need for new ways to ensure that procedures are being done the exact same way each time, or that doctors don’t miss symptoms when they see a patient.

So, whether you heard it here or elsewhere: healthcare is an incredibly complex industry which continues to be plagued by a number of problems.

However, this complexity and systemic distress also gives rise to exceptional opportunities for growth. Researchers, healthcare workers, startups, industry giants, engineers, entrepreneurs, scientists and healthcare enthusiasts all have a shot at transforming many of the existing makeshift solutions and systems into lasting ones.

That being said, a deep understanding of the healthcare system is paramount to contributing to innovation in this industry. That includes knowing the ins and outs of hospitals, big pharma, public health needs, physician workflow, and insurance companies (among many other things).

If you’re looking forward to learning more about how healthcare fits into our socioeconomic fabric and how this sector is positioned to shape up in the coming years, stay up to date with In Fact’s Healthcare Series.